Whether you’re the listing agent or the homeowner, watching days on market rack up with little activity is frustrating. Before taking that price cut, consider financing incentives. These are the top 4 we’ve seen spark buyer interest-for a fraction of the cost of a price drop.

Seller Sponsored 3 Months of Free Mortgage Payments

Attract buyers with the offer to cover the first three mortgage payments.

How it works: We work the listing agent to determine the allowable interested party contributions (IPCs). All or a portion of the IPC may be offered to either cover or contribute to the buyer’s first 3 payments.

Incentive Highlights:

- Builder or Seller contributes funds to cover borrowers’ payment up to 3 months via IPCs

- Funds are held in escrow; the servicer manages monthly payments

- Borrower cannot receive cash back at closing

Some restrictions apply based on loan type, IPC funds available, and borrower qualifications. Check in with me before offering to confirm the dollar amount available for IPC will cover what you’d like to offer.

Seller Sponsored Rate Buy-Down

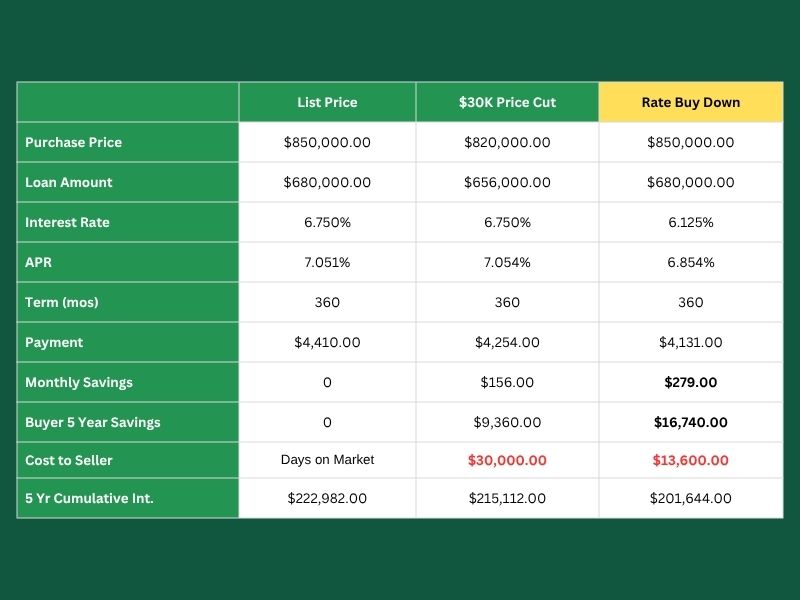

Every dollar toward a rate buy-down provides roughly 3 times the savings to the buyer over a price reduction. This is my personal favorite as it offers the most value for the lowest cost.

How it Works: The seller pays to “buy down” the interest rate. Below is an example that illustrates the power of rate over price.

Example: List Price $850,00. Seller evaluating a $30K price cut. Introduce a rate buy-down; the seller saves $16,400. The buyer saves over $100 more per month!

Incentive Highlights:

- a temporary buy-down (such as a 2/1 or 3/2/1) lowers the rate for the first 2 or 3 years; the rate then adjusts back to the original note rate

- a permanent buy-down lowers the rate for the life of the loan

This scenario reflects a permanent rate buy-down locking in savings for the life of the loan. Scenario provided as an example only. Rates vary with market conditions and borrower qualification. The above is not intended as a quote or offer.

List and Lock

The seller locks a competitive rate up front with Fairway, which can then be advertised to buyers. Lock and list is ideal when rates are on the rise.

How it Works: The seller locks the rate/price for a generic loan scenario.

Example: 80% LTV, 740 credit score, 30-year fixed rate loan.

Borrower specifics that drive loan-level price adjustments may apply and need to be factored into the rate and fees based on the borrower’s actual credit score, occupancy, loan term, and LTV.

Incentive Highlights:

- Fannie, Freddie, and GNMA programs only

- Lock Period: 90 days maximum

- Extensions: up to 30 days allowed

- Rate changes permitted based original lock date pricing

- Up-front $1,500 paid by the seller (refundable if the loan closes with Fairway)

- Must meet applicable seller contribution limits.

- Executed agreement between seller and Fairway

- Required Seller Contribution: 2% minimum applied to either permanent or temporary buydown or closing costs.

Lender-Sponsored Rate Buy Down

Fairway will cover the cost of a 1/0 rate buydown for the first year.

How it Works: A 1/0 buy-down reduces the rate in year one by 1%. For example, from 6.50% to 5.50% on a $450,000 loan amount, the buyer would save approximately $4,500.00 in interest AND benefit from a lower monthly payment for the first 12 months of homeownership.

At the beginning of year two, the rate adjusts to the note rate for the remainder of the loan term.

Example:

- Loan Amount $450,000

- Year one Rate 5.500% (APR 5.85%)

- Year 2-30 Rate 6.500% (APR 6.89%)

(Assumes the borrower qualifies for a 30-year fixed-rate mortgage at 6.50%)

This offer is available on new contracts through September 30,2025.

In a market with more selection available to buyers, sellers who add some creativity and incentive to their property create a more affordable home for the buyer and simultaneously protect a greater portion of their hard earned equity. Financing incentives create a true win-win.