If you’re a qualified home buyer ready to purchase but are deterred by current interest rates and home prices, I encourage you to re-evaluate. Don’t dismiss the data that says buy now.

In a recent broadcast, housing industry expert Dave Stevens offered our Fairway team an insider perspective. Here’s what he shared.

- Home prices will continue to climb for at least the 10 next years as 50 million new buyers enter the market

- Home starts lag demand creating a supply shortfall for the foreseeable future

- Economic indicators support lower mortgage rates

- Owning a home is the single best source of building wealth across all demographics in the United States

Home Prices Will Increase

According to Core Logic, single-family home prices nationwide are up 3.7% year over year. Not alarming, but this follows pandemic home value spikes with no significant compensating drop. The logic behind “don’t wait to purchase” is the realization there won’t be any more significant home price correction. While rates temporarily cooled demand, that is coming to an end. There is no case for waiting in the face of a home supply shortfall and growing demand unless you simply can’t qualify with a higher rate.

Mortgage Rates will Decline in 2024

To follow is a bit of an economic deep dive providing three data points that support a shift downward in mortgage rates. We just need the Fed to cease technical intervention.

Inverted Yield Curve: When the 10-year treasury note yield (a long-term rate) falls below the Fed Funds Rate (a short-term rate), we have an inverted curve indicating a period of recession shown in the chart below as gray bars. The red circles highlight each occurrence and its predictive accuracy a recession will follow. Also note historically, each inverted yield curve was followed by a drop in 30-year fixed mortgage rates. Our existing inverted yield curve indicates a drop in mortgage rates in the forecast.

- Mortgage vs Treasury Excessive Yield Spread: 30-year fixed mortgage rates average 1.75% to 2% higher than 10-year Treasury Securities in a healthy economy. Only in times of economic intervention and recession does this spread grow outside the boundary. Our current spread is approximately 3% indicating mortgage rates are artificially high and will drop when The Fed ceases intervention and allows markets to resume balance.

Put Simply: 30-year fixed mortgage rates are 1% to 1.3% higher than they should be and will drop accordingly when the Fed ceases restrictive measures.

- Inflation Inches Downward: The jobs report for September 2023 shows a shifting job market. The 3.8% jobs gain stems from an increase in part-time jobs including those working multiple jobs with a decline in new full time jobs. Core inflation came in at 4.1% down from the previous month of 4.3% and over 2% below a year ago. Mortgage rates follow inflation in an unrestricted market.

Housing Demand Exceeds Supply

- Pent-Up Demand: A return to lower mortgage rates will unleash pent-up demand from would-be sellers clinging to low rates and buyers priced out of market with rates over 7%. Add to that some 50 million first-time home buyers are coming of age over the next 10 years, and we are about to experience the single largest wave of housing demand in the history of our country. To offer perspective, in 2022 we set a new household formation record with 2.06 million new home buyers. By the end of 2022, estimates showed a 5 million home shortfall in the next 3 to 4 years. An uptick in multi-family structures is the wave of the future to address these substantial shortfalls.

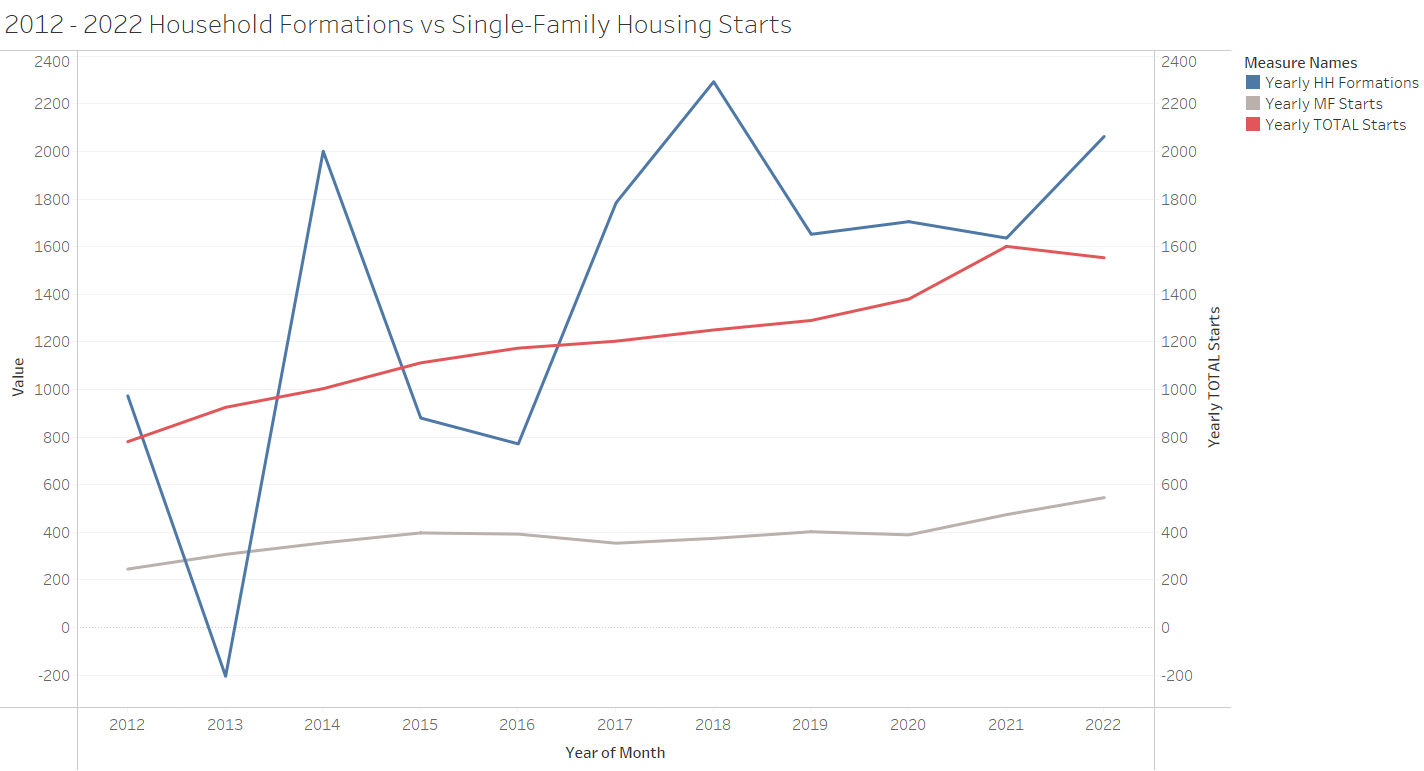

- Structural Undersupply of Housing: Translation-new home starts plummeted following the events of 2008 when everyone with a pulse qualified for a mortgage while population growth continued on and has yet to catch up. Illustrated in the chart below, the U.S. continues to be challenged to offer enough suitable housing to meet demand as new household formations (buyers) exceed yearly home starts (home supply) with no clear end in sight.

Home Ownership Builds Financial Stability

Housing remains the single largest source for creating generational wealth with a sustained average home value annual appreciation of 4.5% for over 4 decades. In boom years, home prices spike to double digit increases. In the downturns, the U.S. has had only one double digit decline, the devastation of the Great Recession in 2008. By 2012, prices rebounded posting a 6% gain and continued to recover in 2013, with an 11% gain according to Core Logic Case-Shiller data.

Over Correction Stalled the Housing Market

The Federal Reserve’s sustained aggressive stance to quell inflation has sparked collective outcry from multiple trade groups and economic experts calling on the Federal Reserve to Halt Rate Hikes. The view that Chairman Powell and the board of governors at the Federal Reserve have “overshot” in their corrective actions is shared widely among industry experts who firmly believe as soon as the Fed formally announces an end to Federal Funds increases, mortgage rates will steadily decline landing somewhere in the mid 6% range by mid to late 2024 and the housing market will light up with activity.

A Case to Buy Now

Waiting to buy a home COULD get you a lower mortgage rate, but waiting to buy a home WILL get you a higher purchase price. We are entering the “slow” season for the housing industry. Now through early 2024 will be your best shot at the lowest home purchase prices for the foreseeable future. Come spring and some much-needed rate relief, competing bids and price increases will likely return. In the meantime, consider a temporary rate buy down-typically a seller-paid concession. You can always grab a lower rate when they come along, but you can’t get a do over on the purchase price.

Data Sources:

Inventory Shortfall Data: https://www.realtor.com/research/us-housing-supply-gap-march-2023/#:~:text=However%2C%20if%20the%20rate%20of,take%20between%202%20and%203

Current Home Price Data: https://www.corelogic.com/intelligence/us-home-price-insights-october-2023/

Housing Supply Data: https://tradingeconomics.com/united-states/monthly-supply-of-houses-in-the-united-states-fed-data.html

Historic Home Price Data: https://fred.stlouisfed.org/series/CSUSHPINSA

{kind=link}