The goal of many retirees and their advisors is to have no mortgage payment once those income-earning years end. Add a move closer to family, a downsize, or a desire for that 55+ community, and retirees can struggle to find that right home that fits their cash budget.

The theory is solid: reducing the monthly taxable income needed to sustain the home, thereby protecting invested assets/savings.

The overlooked alternative to stockpiling cash in an illiquid asset? A reverse mortgage for purchase.

Same end result: no monthly mortgage payment, plus an opportunity to establish a future non-taxable source of cash.

Comparing the Options

Meet Rebecca, age 67, looking to purchase a home closer to family. She has $500,000 from the sale of her previous home.

Option 1: Pay All Cash

Rebecca could use the full $500,000 to buy a new home outright.

While she avoids a mandatory mortgage payment, all of her proceeds now become tied up in the home, limiting her financial flexibility, as her home represents approximately one-third of her overall wealth.

Option 2: Use a Home Equity Conversion Mortgage for Purchase (H4P)

Rebecca could choose to use a PORTION of her cash paired with a reverse mortgage for purchase home loan.

Here’s how the numbers break down:

- $333,910 cash needed upfront to close (down payment + closing costs)

- $166,09 financed through an H4P loan*

- No required monthly principal or interest payments*

- $166,090 in savings preserved

Rebecca has no mortgage payment and a small cash cushion for future needs.

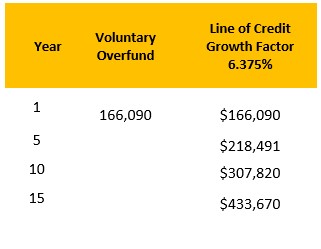

Option 3: The Savvy Tax Strategy of Overfunding the Loan

Rebecca chooses to voluntarily overfund the loan, which establishes a home equity line of credit while simultaneously reducing the loan balance.

Using the $166,090 of preserved savings, Rebecca overfunds her reverse mortgage, creating a HECM line of credit inside the loan. The HECM line of credit now compounds and grows over time at a growth factor equivalent to the note rate on the loan. ( yes you read that correctly, a line of credit that grows without a refinance)

For example purposes, a rate of 6.375%, the current average rate, is applied across the 15-year term shown in the chart. In reality, the rate adjusts each month on the 1-year CMT, capped at 5.%. While the chart only reflects 15 years, the line of credit is available for as long as Rebecca lives in her home, can never be called due, and draws are non-taxable home equity. Learn more here

Rebecca has no mortgage payment, a small cash cushion for future needs, and a home equity line of credit growing safely, tax-free, available to her for as long as she lives in her home.

The H4P creates access to home equity as needed with no required repayment until the home is sold, adding an additional non-income, non-taxable source of funds to her retirement plan.

Meanwhile, the value of her home continues to appreciate, unaffected by any equity draws.