Headlines touting an 11-month low following weak jobs data sum up our mortgage rate environment as we prepare to exit the third quarter.

Fun fact, we had this same twist last September, and it’s taken a year to even get close to the 2024 low. The big question on everyone’s mind: will the trend continue?

Impending Fed Action

As of September 9, the futures market is pricing in a 90.2% probability of a 25 bps rate cut during the September 17th FOMC meeting and a 75.1% chance of an additional 25 bps rate cut during the October 29th meeting (CME FedWatch Tool).

In other words, the impending cut in the Federal Funds rate, the overnight lending rate between banks, is already priced into current mortgage rates.

Mortgage Rates Anticipate

The Fed sets the overnight rate. The rates that influence mortgage rates are longer-term, like Treasuries, not the Federal Funds rate. As markets monitor employment and inflation data, along with the Federal Open Market Committee (FOMC) commentary, they anticipate the future economic direction and price in expectations for longer-term securities, such as 30-year mortgages.

As Chairman Powell stated in August, “we do have an effect, but we’re not the main effect.”

Tariff Uncertainty

To date, most agree that the economic impact of tariffs has been mostly absorbed by the businesses affected and not passed through to consumers. They are, however, a contributing factor to market uncertainty and a pause in hiring, visible in the latest employment figures.

Economists in and outside of the FOMC foresee impending increases in inflation when the mitigation by businesses impacted becomes unsustainable.

In other words, we are either hinging on a downward mortgage rate trend driven by indicators of economic slowing, or we are at a moment of low rates that could vanish in the face of an inflation spike.

The Elusive 5% Rate

There is still no credible near-term forecast of a 30-year fixed-rate mortgage even close to 5%. Economists are all in the wait-and-see camp with volatility baked into current policymaking that directly impacts the financial markets.

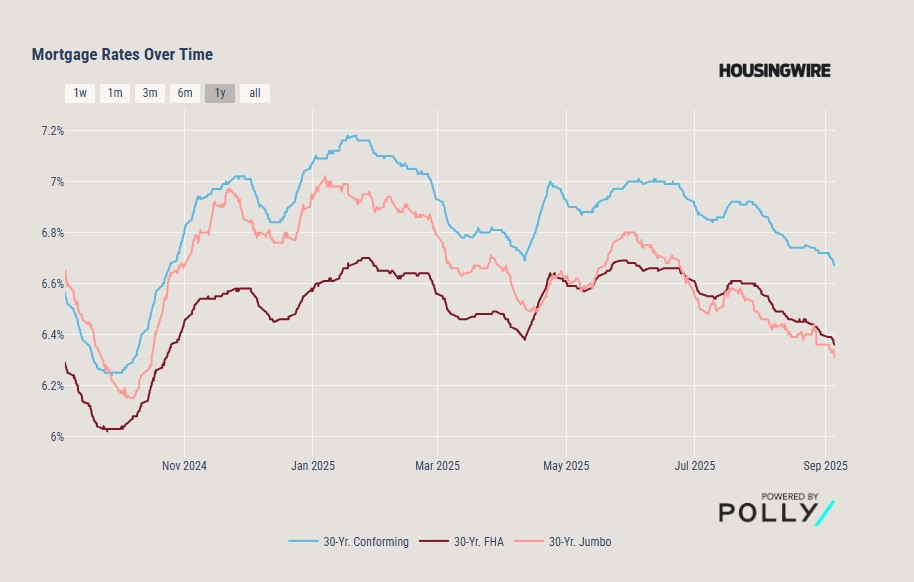

As of noon on Friday, Sept. 5, 2025, HousingWire’s published average 30-year fixed rate was 6.69%. We’re seeing rates range from 6.25% to 6.69% based on the borrower’s qualifying criteria outlined below. Add in a rate buydown, and we reach rates in the 5’s

How to Optimize Your Rate

Your rate is like your fingerprint. What you qualify for is specific to you and depends on:

- credit score

- down payment amount

- loan type, i.e., purchase, refinance, cash-out

- property type

- and the ever-present loan level price adjustments imposed by Fannie/Freddie on conforming loans during the underwriting process.

These next few weeks could be the sweet spot in the market. If you truly want a rate under 6%, the gap has closed, making a rate buydown more affordable and a sure bet. Details on how buydowns work found here.

Written by: Sheila Landis for The Landis Group