Mortgage rates move in anticipation of market actions, and as of yesterday, we hit the lowest point all year. Today, Fed Chairman Powell announced another 25 bps federal funds rate cut, and markets repriced for the worse, pausing our downward momentum.

The September Fed funds cut had the same impact. Why? The commentary. Here’s the recap and some explanation to help position the current and future impact.

Fed Announcement Summary:

- Conclude reductions of aggregate securities holdings on December 1

- The downside risks of employment have increased

- Inflation for goods has increased, inflation for services decreased

- Tariff impact is evident, pushing up prices; risk perceived to be short-lived

None of these comments came as a surprise, though the relative dismissal of current employment reality seems insensitive and short-sighted.

While the market appeared to truly dislike the phrases “policy remains modestly restrictive” and “a December rate cut is far from a forgone conclusion”, the latter comment is what the MBS market responded to.

The December rate cut had already been priced into today’s rates at roughly an 87.3% likelihood as of this morning.

Post announcement reprice has us only slightly higher than yesterday, still comfortably in the low 6’s and into the 5’s with a rate buydown.

Nothing else said or denied offered up cause to believe we wouldn’t continue to see an improving housing market with stable mortgage rates, just not at the pace many would like.

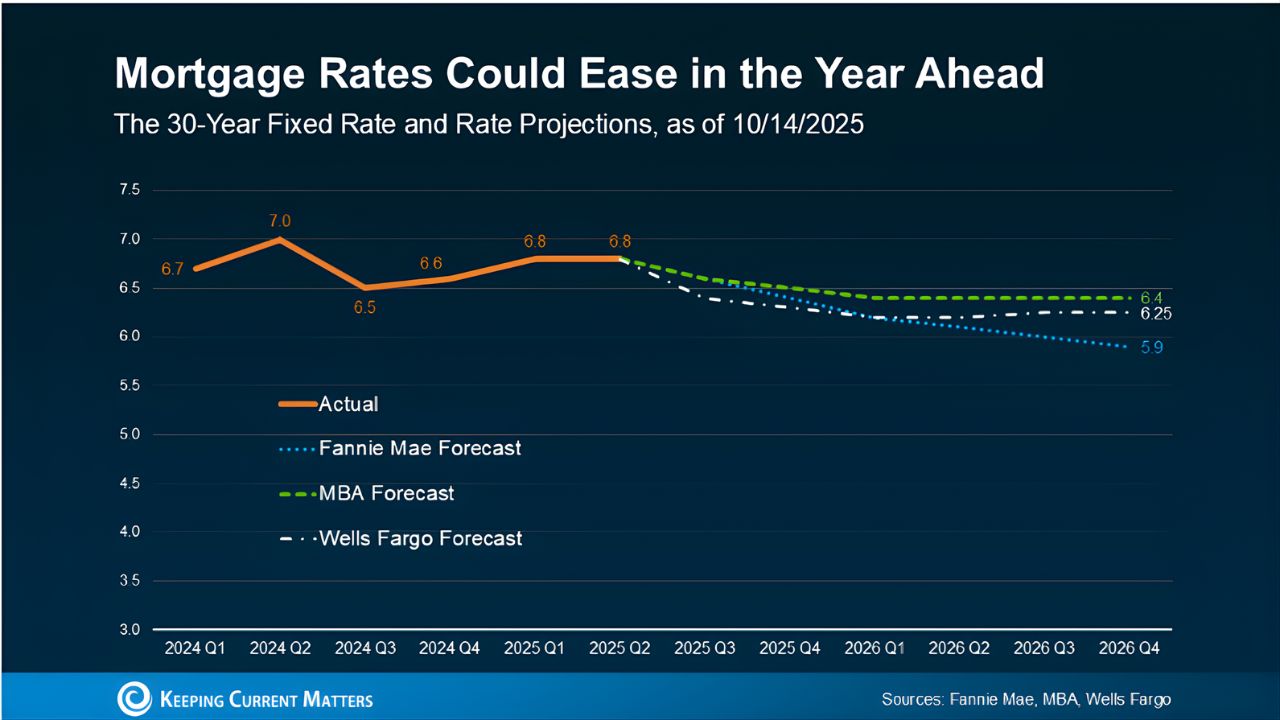

Below is a brief explanation of each bullet and some rate projections through next year.

Fed Balance Sheet

The statement to stop the runoff of the balance sheet is awesome news for mortgage rates. Stated as “concluding reductions of aggregate securities holdings,” it marks the end of quantitative tightening (QT).

Impact: Positive, for lower mortgage rates

Quantitative Tightening is a monetary policy used by the Fed to restrict the economy and cool inflation.

Deployed in March of 2022, the practice has a negative impact on mortgage rates, dampening demand in the secondary markets for mortgage-backed securities, and keeping rates artificially elevated.

While it can be argued that QT helped bring inflation under control, the announcement to end the practice is widely perceived as overdue and welcome news.

It won’t spark a drop, but the absence should further bolster stability and make room for downward momentum.

QE, Quantitative Easing, brought the epic low rates of the last decade and loaded the balance sheet, prompting the boomerang effect, QT. During QE, the Fed purchases and holds mortgage-backed securities, increasing demand and pushing mortgage rates artificially low. (i.e., 2 & 3%)

We are officially returning to market-driven forces, for now. Detailed video explanation of QT found here

Employment & Inflation

Employment – The Fed comment says it all. “Downside risks to employment have increased.” It was followed by numerous data points that were rather soft in light of the continued layoffs, slow decline in manufacturing jobs over several years, and hiring freezes.

It does seem this market force is not weighing as heavily as it should. The headlines over the coming weeks will likely focus on data contrary to Chairman Powell’s view.

Impact: Positive for rates, negative for home buyers facing the uncertainty of future employment.

Inflation – The uptick in inflation through September is tied to goods now pricing in tariff costs. “Tariffs pushing up prices are perceived to be a one-time bump. Risk to be assessed and managed.”

Impact: Neutral for rates, impacting monthly budgets and home buying decisions.

Tariffs

Assuming no additional tariffs are announced, tariff inflation is perceived to be short-lived. Prices will increase, then stabilize. Should prices continue an upward trajectory, that’s a whole new conversation. No restrictive action has been taken based on recent inflation data.

Impact: Short-term neutral for rates, tough on price-sensitive home buyers

Government Shutdown

Great question in the announcement: “Will the government shutdown slow the rate at which future cuts will happen?”

The answer: “If you’re driving in the fog, you slow down.”

Impact: Wait and See

Opposing Forces

From the above forecast, it appears economists have taken to driving slowly as well. Rate forecasts are very conservative and suggest stability with hints of improvement. Historically, the MBA forecasts tend to be the most accurate.

We are at a pivotal point, making rate forecasts unusually difficult. The end of QT and a cooling economy, paired with weakening jobs data, should create a downward trend in mortgage rates and further cuts to the Federal Funds rate.

Key word, should. We also have a government shutdown impeding key data points, combined with the potential for more policy decisions that could negatively impact inflation.

Rates That Start with a 5

Rates continue hovering in the low 6’s and with a small rate buydown, push into the 5’s. More on rate buydowns here

Written by: Sheila Landis for the The Landis Group