Last month, a 68-year-old, recently retired client called me in distress. Her husband has required medical care exceeding their cash flow. Like many clients, the go-to was a Home Equity Line of Credit (HELOC).

Now, she is draining her investment accounts to cover the debt—exactly the opposite of her retirement plan.

This scenario plays out more often than it should. The problem isn’t using home equity in retirement—it’s a powerful tool when used correctly. The problem is not choosing a financing solution that offers available cash today and affordability in the future.

In retirement, you need options that protect cash flow, preserve flexibility, and align with the realities of post-career life. Before defaulting to the old standby, it’s worth rethinking how your home will support your next chapter.

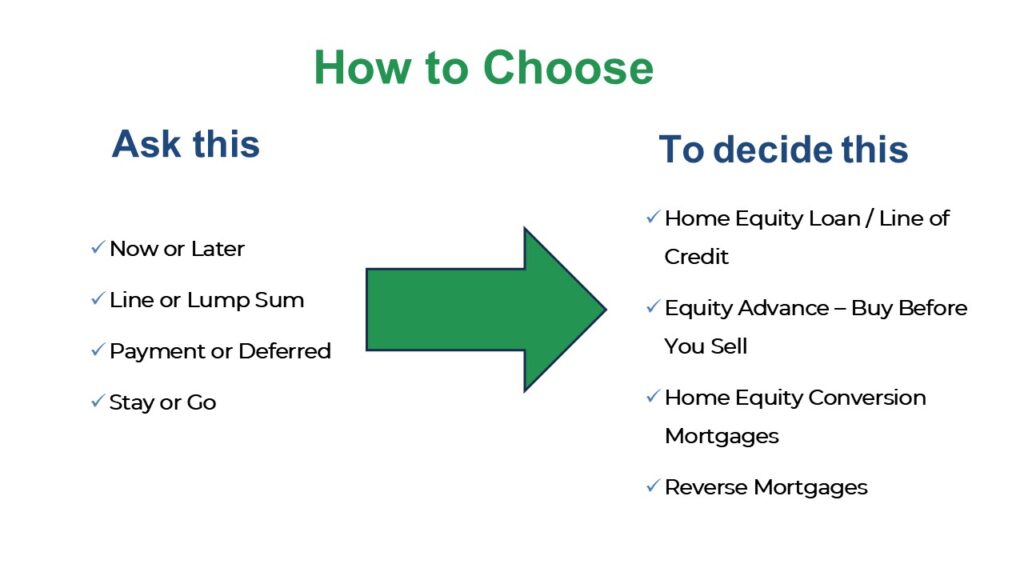

How to Choose

Start with the basic questions to align your financing with how, and for what, the money will be used. I find this approach, paired with a working knowledge of current loan products provides the best long-term outcome.

The Decision Framework

Your responses to the questions below will point you toward the right financing solution and away from expensive mismatches.

NOW or LATER

Do you need money immediately for a purchase or project, or are you establishing a safety net for the future?

LINE or LUMP SUM

Do you need all the money at once for a specific large expense, or would you prefer the flexibility to draw funds only as needed over time?

PAYMENT or DEFERRED

Can your retirement budget comfortably absorb a monthly payment (including potential increases), or would optional/deferred payments better protect your cash flow?

STAY or GO

Are you updating your home to sell soon (within 2-3 years), or planning to remain in this home for five years or longer—possibly for life?

How you answer each question determines which financing product aligns with your plan. A mismatch here is where costly mistakes begin.

Financing 101—Because Everything Has Changed

What you knew about home financing 10, 20, or 30 years ago may be completely outdated. Loan products evolve with market demands and regulatory changes.

Today, lenders like Fairway offer 8-10 different HELOC variations alone, plus an entire suite of reverse mortgage options and bridge loan programs. The choices can be overwhelming without guidance.

This is why working with a knowledgeable mortgage advisor matters. You need someone fluent in all equity-access options who can translate your answers to those How to Choose questions into the right financing.

Equity Loan Line Up:

- Traditional HELOCs — Variable-rate lines of credit requiring monthly payments, typically with a 7 or 10-year draw period followed by a repayment phase. Draw what you need when you need it for the draw period. Note: the minimum draw and payback periods vary by product. Pay close attention to the terms.

- Fixed-Rate Home Equity Loans — A fixed-rate loan with proceeds drawn in full at closing

- Home Equity Conversion Mortgages (HECMs) — FHA-insured reverse mortgages with optional payments and a growing credit line designed for long-term use. Draw only what you need when you need it for the life of the loan

- HECM for Purchase — Reverse mortgages specifically structured for buying a new home, preserving cash, with optional payments

- Jumbo Reverse Mortgages – offered through large private investors, designed to offer a larger portion of home equity than the traditional (HECM)

- Bridge Loans — Short-term financing to utilize equity from an existing home toward the purchase of a new home before you sell

Each serves a different purpose. Your job isn’t to become an expert in all of them—it’s to know what to ask and find a lender who is.

The Familiar Choice Isn’t Always the Best Choice

We naturally gravitate toward what’s familiar deeming it “safe.” Traditional mortgages and HELOCs feel comfortable because we understand them. Terms like “reverse mortgage” and “deferred payment” can trigger immediate dismissal simply due to unfamiliarity.

This brings us to the single biggest mistake I see with retirement home equity: Accruing a large balance on a HELOC prior to exploring better fit alternatives.

🚧 Mistake #1: Using a HELOC (Short-Term Tool) for Long-Term Needs

The scenario: An unexpected roof repair, medical procedure, or family emergency creates an urgent need for cash. A HELOC provides quick access—problem solved, right?

Not if you can’t manage the long-term consequences as shared in the opening client story.

The reality check: Unless you have a reliable income to cover the payments OR a clear plan to pay off the balance within 3-5 years (inheritance, pension lump sum, home sale), a HELOC can quickly become unmanageable on a fixed retirement income.

When a HELOC Is Too Risky for You:

☐ You cannot comfortably afford the monthly payment if rates increase by 2-3%

☐ You don’t have a specific payoff plan within 5 years

☐ You’re using it for ongoing expenses-medical bills, living costs, home maintenance

☐ You’re already concerned about outliving your savings

If you checked any of these boxes, a HELOC may be the wrong tool.

HELOC Reality Check: What You’re Actually Signing Up For

Let’s get specific about how HELOCs work.

Typical Structure:

- Draw period with interest only payments: access to the line of credit, usually 7 to 10 years.

- Repayment period with principal + interest payments: once the line closes, payments increase, significantly if the repayment period is short, i.e. 3 or 7 years vs 20 years.

Payments Increase over Time:

Consider a $50,000 HELOC at 8.5% during the draw period. Your interest-only payment is roughly $354/month—that’s $4,248 annually from your fixed income.

Now imagine:

You enter the repayment period → Your payment creeps up again to include principal and interest. Based on your repayment period, that monthly amount jumps to $466/mo. on a 20-year repayment period or as high as $791/mo. on a 7-year repayment period.

Can your retirement budget absorb that? If not, you’re looking at rapid depletion of savings or worst case, selling your home—the exact opposite of your retirement plan.

HELOCs Make Sense When:

- You’re completing a home improvement before selling at which time the loan will paid off

- You need short-term flexibility and have income and assets to support payments

- You can genuinely afford payment increases without financial stress during the repayment period

🚧 Mistake #2: Choosing Based on Upfront Costs Instead of Long-Term Fit

Using the decision framework from above to drive your conversation avoids mistake #2, making a decision based on rates and fees. The cheapest upfront cost options, often associated with a short-term need loan, don’t necessarily translate to the most affordable choice over time.

The mistake: If this is a long-term play (staying in your home, ongoing expenses, uncertain timeline), that’s an expensive retirement spend down misstep.

How to avoid it: Match the loan structure to your timeline and purpose, not just the initial fees. A product that costs more upfront but offers payment flexibility and rate stability may save you thousands over time and protect your ability to stay in your home.

Note: for many retirement mortgages, the costs to establish the loan are wrapped into the loan, limiting your out-of-pocket expense.

🚧 Mistake #3: Avoiding Reverse Mortgages Based on Outdated Information

A reverse mortgage can be dismissed as an option for any number of reasons including the perception it’s for those who didn’t plan well, it’s a scam, you sign your home over to the bank, or your heirs will inherit less.

Modern Home Equity Conversion Mortgages (HECMs) are heavily regulated FHA loans with consumer protections that didn’t exist in earlier generations. Used strategically, they’re often the safer option for home equity access in retirement.

Secure your estate with a modern reverse mortgage:

- Slow the spend down of savings and investments, weaving in home equity

- Plan for in-home care and ongoing home maintenance

- Protect access to equity: borrowers exclusively hold title and the access to available equity. They may sell at anytime, payoff the balance, and walk away with the remaining proceeds – it’s a mortgage

- Affordably remain in or purchase a home: financing designed specifically for those aged 62+

- Protect estate value leaving a well maintained home, move in ready for your heirs or a hassle free sale when you’re no longer living there

- Retain independence with the built-in, payment deferred, growing line of credit option; aka, the too good to be true part

The Strategic Alternative: Home Equity Conversion Mortgages (HECMs)

Access & Flexibility

- Provides ongoing access to home equity—draw only what you need, when you need it

- The line of credit grows over time without requiring a refinance

- The loan can never be called due or frozen as long as you live in your home, pay property taxes, insurance, and maintain the property

- Money can be drawn out and paid back as often as you like

Financial Benefits

- Accrue interest only on funds actually used, not on available credit

- Draws are not reported as income, are non-taxable, and typically don’t affect Social Security or Medicare

- Lower interest rates than HELOCs

- Can be used for any purpose: home repairs, medical expenses, daily living, travel—anything

Payment & Ownership

- Payment is deferred until you sell your home or pass away, though you can make voluntary payments anytime to reduce the balance

- You retain full title to your home at all times

- You can refinance or sell whenever you choose

- All remaining equity belongs to you and your heirs

Protection Features

- Non-recourse loan: If the loan balance ever exceeds your home’s value, you (or your heirs) are never responsible for the difference—FHA insurance covers it

- Required financial counseling ensures you understand the product before committing

- Only borrowers named on the loan have access to the money

- Loans can close inside of a Trust

- Credit line can never be frozen or expire

Real-World Impact:

That same $50,000 drawn from a HECM instead of a HELOC means:

- Zero required monthly payments = $4,200+ annual cash flow preserved

- No payment shock when repayment period arrives

- Flexibility over time any money paid into the loan is retained in the line of credit, continues to grow, increasing your available cash position and may be drawn back out at anytime

For a retiree on a fixed income, preserving $4,200-5,000 annually in cash flow while maintaining access to funds is often the difference between financial security and stress.

Protecting Your Family’s Future

Here’s a scenario many don’t consider: What happens to your heirs if you have a traditional mortgage or HELOC and can no longer make payments?

Traditional Mortgage/HELOC:

- Payments are mandatory every month

- If you’re incapacitated or pass away, your heirs must continue payments

- Creates a potential financial burden during already difficult times

HECM:

- No mandatory payments during your lifetime

- Heirs inherit the home with time to make decisions (typically 6-12 months)

- Heirs can pay off/refinance the loan balance and keep the home, or sell and keep all remaining equity

The non-recourse feature matters: Your heirs will never owe more than the home’s value, regardless of the loan balance. This protection doesn’t exist with traditional financing.

The Power of Planning Ahead

You don’t have to use a HECM immediately after establishing it.

In fact, one of the most strategic moves is setting up a HECM line of credit before you need it—establishing it in your 60s or 70s, giving the line of credit time to grow before money is needed.

Why?

- The balance in the line of credit grows every year (typically 4-6% annually)

- A $100,000 line today could be $160,000+ in 10 years

- It’s there if you need it; untouched if you don’t

- All draws are non-taxable home equity dollars

Think of it as “equity insurance”—protection against future unknowns like market downturns, health crises, or outliving your savings.

Making the Right Choice: HECM vs HELOC

The goal: Safe, strategic use of home equity with a financing structure that protects your retirement cash flow while giving you the access you need.

Your home equity is a powerful resource. When paired with the right financing strategy, it can extend and enhance your retirement lifestyle. When mismatched with your actual needs, it can compromise everything you’ve built.

The Client with the HELOC

My new friend going down fast under her new debt burden, came up short to close on a HECM as her home financing debt exceeded the portion of equity available to her.

- Her decision-pull the small shortfall of $6800 from savings to close the gap.

- The outcome– payment on $170K for the first and second mortgage debt is now gone, saving $2,270 per month.

- The impact – life changing.

Matching the Need to the Loan

Responsible use of home equity will always make sense—your home continues to appreciate regardless of what you borrow against it. The key is matching the financing tool to your actual situation:

- Short-term needs with clear payoff plans → HELOC works well

- Long-term needs, staying in your home, limited income flexibility, balancing retirement spend down → HECM protects you better

- Uncertain future needs → HECM line established early grows over time

Plan ahead. Learn about your choices. Ask questions. And work with a mortgage advisor who takes the time to understand where you’re going, not just where you are today.

Your retirement security is worth getting this decision right.

Additional Resources:

A Consumer Guide to Reverse Mortgages

A Consumer Guide to Purchasing with a Reverse Mortgage

Written by: Sheila Landis for The Landis Group