The term gets thrown around a lot, but just exactly how do they work, when should they be used, and who benefits – buyer or seller?

Read on and learn the anatomy of a rate buydown.

Types of Rate Buydowns

Rate buydowns come in two forms: temporary and permanent. The best choice depends on the needs of the buyer, the seller, and current market conditions.

Comparing the Options

- a temporary buy-down (such as a 2/1 or 3/2/1) lowers the rate for the first 2 or 3 years; the rate then adjusts back to the original note rate

- a permanent buy-down lowers the rate for the life of the loan

Temporary Buydowns

A temporary buydown lowers the initial rate on the loan for the term of the buydown, after which time it adjusts to the full note rate.

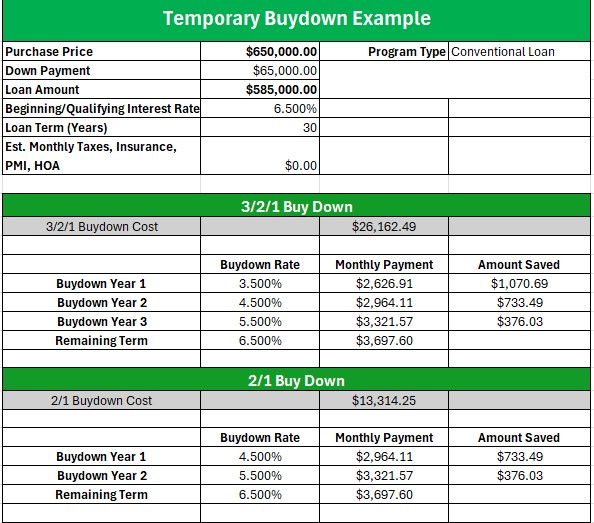

The most common is a 2/1 buydown where the interest rate is 2% lower than the note rate on the loan for the first year, then 1% lower for year two, adjusting to the full note rate at the beginning of year three. In this case, the term of the buydown would be two years.

The numbers below bring the savings to life, with examples of both a 2/1 and a 3/2/1 buydown at a purchase price of $650K with a 10% down payment.

The column titled “amount saved” reflects the monthly savings at the temporary lower rate.

The Win-Win Seller Incentive

Including a temporary rate buydown as a seller incentive saves a new homeowner thousands in their first years of homeownership while preserving the asking price for the seller.

Candidates for a Temporary Buydown

- Seek a lower payment in the first couple of years to accommodate paying off other personal debts to reduce overall monthly expenses

- Are anticipating higher future income to support a higher payment at the end of the buydown period

- Are open to refinancing to lock in a permanent lower rate in the future

An added bonus with a temporary buydown: if the loan is refinanced during the buydown period, any unused buydown funds are applied to reduce the principal balance at the time of the refinance. In other words, you don’t lose those buydown dollars inside the window of the buydown term.

Note: the buyer must qualify at the full note, not the lower opening rates. A temporary buydown does not assist in qualifying for a higher loan amount.

Permanent Buydowns

Permanent buydowns lower the interest rate for the entire term of the loan, typically 15 or 30 years.

Familiar with the term discount points? That refers to the one time fees paid by the borrower or the seller toward loan costs. A rate buydown is simply an added fee, defined as discount points, that reduces the current note rate to a lower, below-market rate for the life of loan.

There isn’t a most common percentage or cost in the case of a permanent buydown. It is case specific with buyer goals at the forefront of the decision criteria.

Exploring buydown options before making an offer can inform how that offer should be structured and determine if a seller contribution is needed to achieve the desired outcome.

Candidates for Permanent Buydown

Need to qualify for a higher loan amount

- Plan to stay in the home through and beyond the average financing payback period of 2-3 years

- Can still fund an adequate down payment for the chosen loan type

- Prefer to pay more up front for long-term savings

- Seek to avoid refinancing, which drives a new set of closing costs

- Don’t like uncertainty. Would rather establish the preferred lower monthly payments upfront

Who Pays?

The funds to cover the buydown, whether temporary or permanent, can come through seller concessions (assuming there is room in the allowable contributions, which can be 2-6% depending on loan type), the buyer, or as a lender or agent-sponsored promotion.

The most common is a seller sponsored promotion attracting buyers to their home, preserving the asking price, and saving the new homeowner thousands of dollars over the life of the loan.

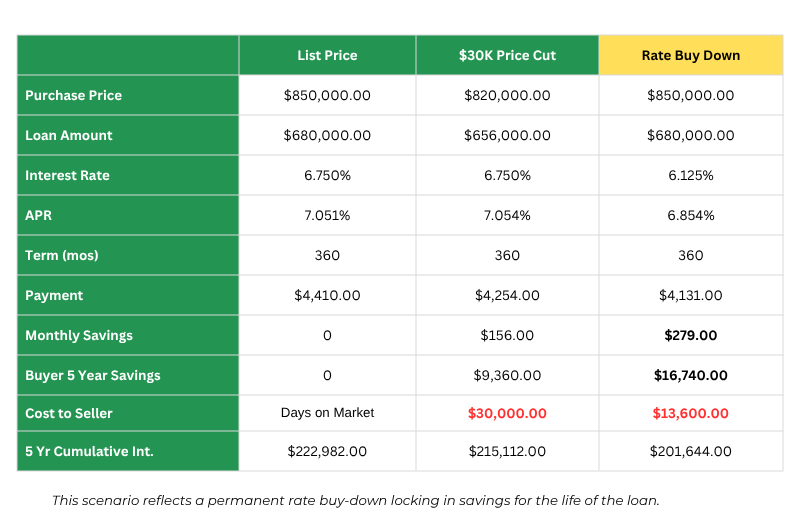

Seller Sponsored Buydown Example

How it Works: The seller pays to “buy down” the interest rate paid in points as a seller credit in closing.

Client Scenario:

- List Price $850K and the seller is evaluating a $30K price drop.

- Swap that for a rate buydown; the seller saves $16,400. The buyer saves over $100 more per month.

- Supports qualifying for a higher loan amount for the buyer

Permanent Buy Down Example

Eliminate the Cold Feet

A rate buydown can eliminate the cold feet many buyers get when they feel there could be future rate actions right around the corner that will offer them a” better deal”. Redfin recently published statistics on this phenomenon, and it’s devastating for those trying to plan a move.

Rates under 6% have been forecast since mid-2022, and we’ve yet to get there without a buydown. Savvy buyers and sellers with experienced agents have learned how these work and when to use them, sparking activity for listings and affordability for buyers.

Create an incentive and add some savings to your next home purchase or sale; consider using a rate buydown.

Note: all numbers presented here are for example purposes only and do not constitute an offer.

Written by: Steve Landis for The Landis Group